Ok, so something has been bothering me ever since I started thinking about housing in an economic sense. Housing prices seem to consistently rise faster than inflation over long periods (at least in large/medium metros). This means that housing is currently more expensive to people than it was 30 years ago. So what happens 50 years from now? or 100 years from now? Who will be able to afford to buy a house? Will people spend more than 50% of their take-home pay on mortgage payments? This doesn't seem sustainable long term.

Thank you for those links. My underlying assumption was that wages grow close to inflation, but obviously that may not be the case, so getting direct wage numbers is much better. Its interesting that the home price to income ratio is climbing back up after the recession. It looks a bit ominous.

> Who will be able to afford to buy a house? Will people spend more than 50% of their take-home pay on mortgage payments? This doesn't seem sustainable long term.

The US housing market is open to bidding from the richest people in the world. Wealthy people in other countries see US housing as a good way to store value, and are driving up housing prices. To answer your question: while Americans will be priced out of the housing market, wealthy people from across the globe will continue to buy into it.

Can someone point me to statistics about this phenomenon? It sounds true that foreign investors use US housing as an investment and inflate prices, but I have no idea how large this effect is.

For reasons pointed out by another reply to your comment, it's difficult to quantify. Anecdotally, I live in newer construction in a suburb of Seattle. At first the neighborhood was populated by local people who live and work here. As the original buyers have been moving out of the neighborhood over the past 5 years, the buyers of literally all been foreign Chinese. All of the houses surrounding mine are now occupied maybe 50% of the time, and I see luxury cars with Chinese license plates parked in front of these houses all the time.

There may not even be statistics - Canada doesn't have any comprehensive foreign demand data - that accounts for multi-unit demands for recent immigrants (now citizens or PR) acting as proxy buyers for third parties to evade taxes, and various other reporting gaps that exist.

So it mostly comes down to relative wealth & population sizes versus desirability of an area, and then spillover effects into surrounding areas. But unless China crashes I would expect this to be an increasing source of demand over time, especially if you live in a pro-immigration country that needs to paper over domestic government budget shortfalls.

That's basically the direction, yes. It's like healthcare in the US: Since people can't opt out of it, the system continuously optimizes for taking as much of their income as possible for the same good.

I started shopping for a home a few years back, and I noticed something interesting: prices had adjusted so that the total cost of owning (including mortgage interest, taxes, maintenance costs, etc.) was almost exactly the same as the total cost of renting! It didn't matter what I did; the choice had been reduced to "Do I want to make a leveraged bet on the housing market, or not?"

I did. That bet was basically a wash when I sold last year. After final calculations... I paid within $100 a month of market rent for the place.

The only way you can get out of the trap is to acquire enough cash to simply buy outright (and then hope you never get the itch to move). And, of course, then that money is locked out of the investment market.

I did that a long time ago (not in the US) and owned the place until a few years ago, when I radically misjudged the market and ended up selling it at the bottom. Oops.

Now I own a nicer and much more valuable place, with a mortgage; I may be able to keep it and pay it off, or I may have to sell if I ever want to move.

For me personally, the lesson was that I want to own outright, or if I can't do that then rent, and I think I can do that for the rest of my life subject to some obvious limitations.

Mostly because of the mobility trap presented by a mortgage.

>It's like healthcare in the US: Since people can't opt out of it

We do not have a national healthcare system as most of the world does. We are not forced to have healthcare. Yes there are provisions of Patient Protection and Affordable Care Act that charge a tax penalty if you are not covered or exempt.

I always thought the bet is not rent vs mortgage, but whether or not you can sit out the mortgage. Of course it's cheaper to rent if you plan to sell within twenty years.

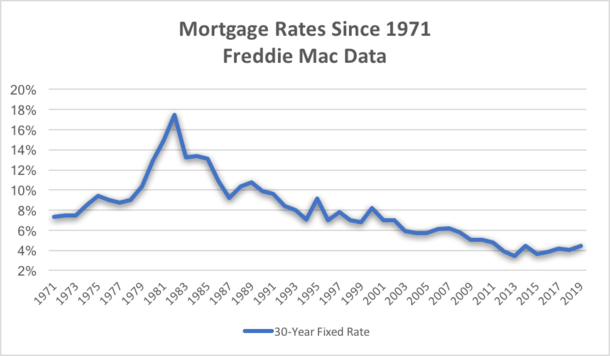

It's true that housing is getting ridiculously expensive. But there is a side that's often not really told, or really explained well, which is interest rates dropping consistently and hard.

(ignore the weird domain, there's plenty of similar sources).

Fact is that rates used to be as high as 18%. Recently they've gone as low as 3.5%.

Real estate is hugely debt-driven, and the standard mortgage contract is set for 30 years. Thereby 'housing costs' isn't really reflected in just the price of a home, as say, the price when you buy a banana, which you buy instantly with cash. Instead, housing costs are dominated by the financing costs, which you pay for over the course of 30 years.

Those housing costs have price as a major factor, sure, but it's multiplied by interest rates. You can't leave that out of the historical context. And if you do, housing costs have in fact not increased quite as sharply as people think.

To illustrate, a $100k home with 3.5% vs 18% rates over 30 years, will cost $160k vs $540k.

In fact, a $333k home at 3.5% rates, will require total payments equal to a $100k home at 18% rates, both around $540k. In short, prices could have tripled since the height of the mortgage rates until the bottom, and yet, you'd have made exactly the same total and monthly average payments.

We often get shown price to income graphs getting worse and worse. But that doesn't capture the reality: monthly payments aren't getting nearly as bad, as interest rates have dropped hard. Higher prices are easier to pay off.

That's not to say that housing isn't getting more expensive, it is. But if you correct for inflation (i.e., average income growth) and correct for much lower financing rates (lowering monthly payments), it's not nearly as bad as is often presented.

An easier way to look at this is the percentage of money we spend of our income on housing. You can see it's on the rise, but really, it's not as extreme as some would think. None of the doubling-tripling kind of figures about housing you see in the media.

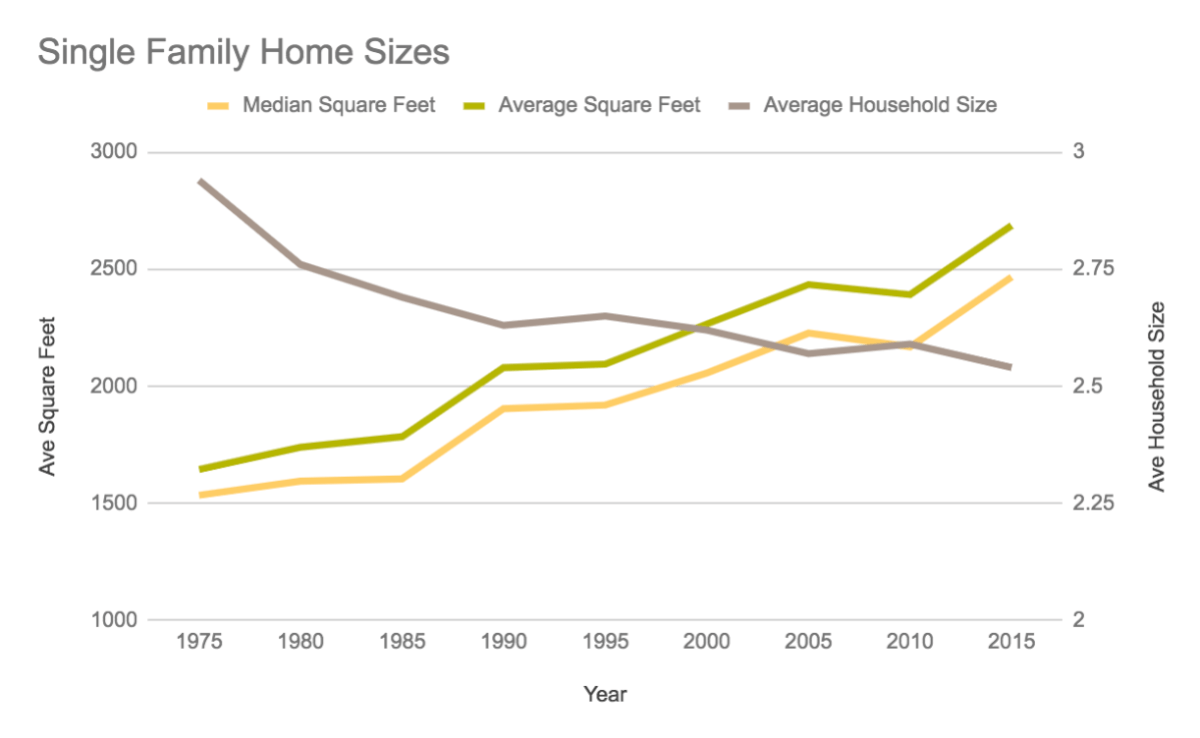

Then lastly, we're just looking at how much we spend, not at how much we get in return. Suppose phones got more expensive, nobody would bat an eye, the phone today is 10x the phone of 20 years ago. What about housing? Here too the data is a bit tricky to get, I'd love to see more research on this. But there are some figures about average home size:

The average home size grew from 1500 to 2500 square feet, while the average household size decreased. In short, in part 'housing' is not getting more expensive itself, but rather we're purchasing more of it, thus spending more on it. If you correct housing costs (i.e., bring it back to a $ per unit of house size), the growth is also much lower.

If you take all this together, then housing is still getting more expensive, but most places are not all that much worse than many years ago. That's not to say we should ignore this as a policy issue, I think it demands lots of attention. But I do think the media narrative and vox populi currently is blind to the other side of the story and only has one message: extreme prices, unseen crisis, lost generation, no hope, etc.

This is very important, especially when discussing it with people who rent. People who are paying 3000-3500 a month looking at a 1 million dollar house as something insane (well, it is, sorry I'm just using round numbers to make it easier for myself).

But depending on interest rates and property taxes, these might be almost the same thing, or very close. Once you consider the portion of the mortgage that goes to the principal, and if you assume some amount of inflation and increase in value, the 1 million dollar home might be cheaper, even if you consider that you could have invested the money in S&P (in this particular example the market would have to be in a fairly ideal state to favor the mortgage, but still, it's close, and you get to make holes in the walls without anyone bitching about it).

Homes are this expensive because, for better or worth, they're worth it. That's the problem. As long as they are worth it it will keep going up (and rentals as well as infamously AirBnB are making sure they're always worth it unless you push out an INSANE amount of supply, where incremental boosts in house building, rent control and affordable housing initiatives may make things worse rather than better.

What your analysis doesn't take into account is that if interest rates go up, demand plummets and the 1 million dollar home at 3.5% is worth 600k at 10% interest rate.

A big RE mogul used to say "Its better to buy a cheap house with expensive credit than an expensive house with cheap credit. You can refinance the latter"

When you have a $300k loan and refinance midway from high to low or low to high interest you will pay the same amount of interest in the end. The reason why low interest rates are bad is because everyone is bidding prices up. Paying $1000k at low interest for the same house is fundamentally worse than paying $300k at high interest.

Sure, but in the markets people bitch about that hasn't happened. Even during the crash, prices didn't move downward that much. There is a risk for sure, but that's true of all investments that pay better than t-bills.

We've seen a shift of preferences towards externalizing the risks of asset ownership to third parties. Many people today prefer to purchase a stake in a real estate conglomerate, and contract out the maintenance and labor, rather than own an apartment building outright and operate it themselves. It's an attractive option for the owners, but carries the risk of creating bureaucracy for the renters.

I think if we continue in this direction, we'll see a resurgence of co-op style ownership, where no individual can afford to purchase the 4 story brownstone in Brooklyn, but a board of 4 shareholders can.

If you want to buy a house for yourself to live in, you might be purchasing a vanishingly-small set of "living-rights" shares from a conglomerate. You won't have to pay for your hot water heater, but you won't have the right to repair or fix it yourself.

> If you want to buy a house for yourself to live in, you might be purchasing a vanishingly-small set of "living-rights" shares from a conglomerate. You won't have to pay for your hot water heater, but you won't have the right to repair or fix it yourself.

Life, Liberty, and the Pursuit of Happiness -- that's all you get. For everything else, you gotta pay.

One significant aspect of increasing house prices is increasing house sizes, amenities, and services (from an HOA). People keep buying more because they think they need it, and I think a return to spartan living would do well for the country but I don't see that happening for a variety of reasons.

The price of assets is directly related to interest rates. This relationship is obvious if you think about it. People borrow money cheaply, the more money that's available, the more money people have to bid up prices of assets. The way interest rates are (including negative interest rates across the globe) I doubt there will be a curb anytime in the future. The biggest unknown IMO is related to the status quo. Perhaps people will value freedom more than security and therefore won't chase those housing values.

For a growing city a house changes in definition. Eg in new cities houses are a 1/4 acre, then they get subdivided then eventually apartments. So the land can keep going up faster than inflation/wages and still a housing unit remains (relatively) affordable.

Also medium term affordability fluctuates so when a boom ends you often get 10 years of flat prices so its a drop after inflation.

Rent is probably cheaper than ownership, except for the investment component. Because the market isn't efficient here, and because of the asset growth, owners can get a positive return even if rent doesn't pay the full mortgage.

the "rule of thumb" is to rent out for 5% (per annum) of the price of the property. This is the unrecoverable cost of owning a property - 1% in maintenance, 1% in

property taxes, and lastly, the cost of capital (which, i've set it at 3% as an estimate).

If your rent is exactly 5%, then the landlord is cashflow neutral, and the property appreciation is what the landlord gains. If your rent is below 5%, it's a good deal, and if it's above 5%, you're getting shafted by your landlord.

Interesting. I have not heard this rule before (and I assume it's modified by the actual tax rate).

That said, unless the local real estate market is strong I don't think it makes sense as an investment to break even on the rent. It's a lot of headache and risk to bet on a >5%[1] average annual appreciation. I don't think that is a reasonable rate to expect in many (most?) real estate markets.

but TLDW; the unrecoverable cost of rent is just the rent money, and a lot of people compare it with a mortgage incorrectly. A mortgage is not 100% unrecoverable, but some portions of it is unrecoverable (the interest). The other unrecoverable cost of owning is the initial downpayment.

The 3% capital cost is the combination of the above interest payment and the lost income opportunity from the downpayment. Whether you buy out right with cash, or get a mortgage, you still end up paying a price either way (via interest, or via lost opportunity to deploy the cash downpayment).

That assumes a hot market where values are riding quickly. The math doesn't work very well if the value growth is around the typical 3% per year.

Also, if the value of appreciation really is that high I don't think it is correct to leave that forfeited value out of the "renting is cheaper" equation.

First, that's not entirely true. We just moved out of a half-duplex that we could have bought if we wanted to (the owners decided to sell it near the end of our lease term).

Second, in the case they are different kinds if properties, comparing them on cost alone isn't valid.

Yes, that was my point. Saying that renting is almost always cheaper than buying when the properties for rent are inferior to the properties for sale is meaningless. Renting the properties that are worth buying is not almost always cheaper, except in certain markets at certain times.

As someone else pointed out, people from all over the world, not just people who want to live there, can buy a house. That means a LOT of people can afford them even if they were a few times more expensive.

Still, the majority of homes are still either bought by people who plan to live in them, or by landlords who will rent them to people who will, so obviously some people can afford them.

Turns out, doctors, a subset of lawyers, various other high end professions including, yes, software engineers, make a lot of money, and there's quite a few of them. Add couples and families and you don't need everyone in the home to be able to afford it, either. Roommates can split the bills. DINKs end up with much more disposable income that can seem astronomical to more traditional families. Older people may have been able to accumulate wealth that seem impossible to 20something or even 30something years old. You can add a lot to that list of examples.

Even when you take away all of the outliers (like rich Chinese investors), turns out a shitload of people can afford these places (which is why if you want to use supply to reduce prices, you need to build a LOT before it goes down enough to reach the lower and lower middle class).

Also consider that 50% of your income (in an investment, no less!) when you have a family income of 250k isn't the same as when you have 50k. I'm fairly privileged, and if I gave up 50% of my income to housing (with a large portion really being a stored investment), it would still make a ton of sense financially.

For sure it shouldn't be that way: even if you were a rich selfish bastard, its easy to see how the people you're displacing are going to come back and be a pain in your butt (see San Francisco), so it's in everyone's interests (not just for social justice) to fix this problem. Still, it's this expensive because it's still worth it and there's still a ton of people who can afford it.

It really dawned on me when I last looked at the status of my mortgage and my savings. When I bought my place less than decade ago (so not as expensive as the market is today, but still when the market was red hot as the interests were at an all time low), it was a non-trivial percentage of my income, the downpayment was most of my savings, and we were definitely running the numbers to see what would happen if my wife or myself lost our jobs. It was tight. A few promotions, job changes, and favorable economic conditions later and I could almost pay cash if it was still at the same price it was back then. Early 30s me thought it was an insane amount of money, but 40something me wouldn't have much issue with it. That's the kind of economic reality and competition we're dealing with here.

turns out a shitload of people can afford these places

Yup! I noticed that in the SF market. With all the tech, biotech and finance jobs here, there are a lot of households with incomes in the $500K range or ~$25K per month after tax income.

A $1.5M mortgage is ~$6K, maybe $8K total including taxes.

That's only 33% of take home income for this hypothetical household.

I'm not on the west coast but was just reading an article a out the entry level salaries for software engineers at top tech companies in the Bay area. Many are really close to the numbers you used in your example, so it's well within the reach of these people if they are DINKs before they are in their 30s.

So to make a dent in the market price you need to have more supplies than there are tech folks. That's a lot.

Don't hold your breath. Kind of hard to find the exact figures, but median home equity is somewhere in the range of $30-150K. (Probably per-household, so divide by two?)

I'm sure substantial transfers do happen, but I've never met anyone that was so lucky.

The relevant figure is median home equity at retirement or potentially age of death.

The overall median would include 20-30 year olds that have only a deposit, 30-40 that are still paying it off, etc. They're not handing down anything for another 20+ years.

> HELOC's to pay for their assisted-living. So the transfer is from boomers to doctors

Eh, I did some work for nic.org. Assisted living is a real estate game, and the market reports are identical to apartment market reports. The medical bills go to Medicare and private insurance. Doctors aren't getting rich off Granny reverse mortgaging her house. Unless said doctors own an assisted living facility, preferably in one of the 30 major MSAs. I vaguely recall Florida being particularly attractive.

True, not HELOCs. I was thinking of Medicaid spend downs there.

It's been a few years since I've looked at it, but if you needed nursing home care, the typical advice was to spend down your assets in a hurry to qualify for medicaid. And in some circumstances, medicaid could put a lien on your home for post-death repayment of services.

Houses keep getting to be better quality. 30 years ago, houses were smaller, built with shittier materials, cost more to heat and cool, didn't have as many bathrooms, appliances, or wiring.

None of this is free.

Houses should be outpacing inflation under these conditions.

This is complete nonsense are at the very least, localised to you and you region.

2 bedroom, shitbox, shoe-box apartments are being sold for $1,000,000 in Sydney that are being condemned less than 10 years after they were built because of the shocking quality of their construction.

I'd go further than that, and say most of Metropolital Australia is the worst example of a bubble.

```

Over 66% of Australians live in the greater metropolitan area of Australia's 8 capital cities with Sydney being the largest (around 4.9 million), followed by Melbourne (4.5 million).

```

> Housing prices are driven by the people paying the price

Not sure how that relates to the Ricardian theory, but while prices are technically "driven" by the people paying them, this does not seem like a useful observation to me. This isn't "if you keep buying every next more expensive iPhone, Apple will keep raising the price". You can't just not buy/rent property. It is a basic necessity.

While prices vary between regions, that is still hardly a choice. Most places, jobs are scarce and transport is a disaster - you can't just go live somewhere else because your job is here (and most jobs are in high-rent areas).

This means that no matter how high* prices get, people will have to find a way to pay (even if that means basically starving for the rest of their lives) and landlords are aware of this, so they keep raising the prices with the argument that "people clearly have the money, so it's fine".

In theory, it makes sense for a finite resource to increase in price with increasing demand, but prices are increasing a lot faster than demand is and housing isn't as finite as land is (we can build up). This points to the supply side (landlords and developers) being the problem, not the people just trying to survive.

With the birth rate dipping, I'm wondering if this will self-correct when the baby boomer generation dies off and there is a larger supply of housing per capita.

It'll just go to their children and accelerate some fun inequality problems

eg: living in fancy inherited house with no mortgage but way out of your price range based on income. The "real" cost of the house then isn't what it's worth but what your taxes come out to be...

In California property taxes are not re-evaluated when a property changes hands by inheritance. So, they really aren't paying anything close to the actual value.

Which, lets admit, is just plain ridiculous. Prop 13 needs to be repealed or at least severely amended. Right now it is a wealth transfer program from the poor to the rich.

As more wealth is tied up in houses and houses are passed on to children, owning a house will become even more dependent on the wealth of your parents than your income.

Someone with a house they pay low taxes on but is worth several millions is unlikely to sell so housing prices will keep shooting up and exclude many people who simply weren't lucky enough to be born to richer parents.

But the trend is also that there are more people per household. I.e. I don't know that we can say that it's a 1:1 relationship that as the population grows so does the number of houses needed.

{kind=link}

{kind=link}

{kind=link}